Full Steam Ahead In the Strait of Hormuz? Not So Fast

The situation around the Strait of Hormuz remains uncertain

On June 17, the US and Iran signed a 14-point memorandum of understanding (the “Islamabad Memorandum” or MoU). This set up a 60-day extension of the ceasefire, specifically intended for drafting a permanent treaty. The agreement committed both nations to an immediate and permanent cessation of military operations on all fronts. Another step was the immediate toll-free reopening of the Strait of Hormuz and the lifting of the U.S. naval blockade. A little more than a week after the agreement was signed, we can take stock of what has transpired so far as expected and which developments have surprised the oil and tanker markets.

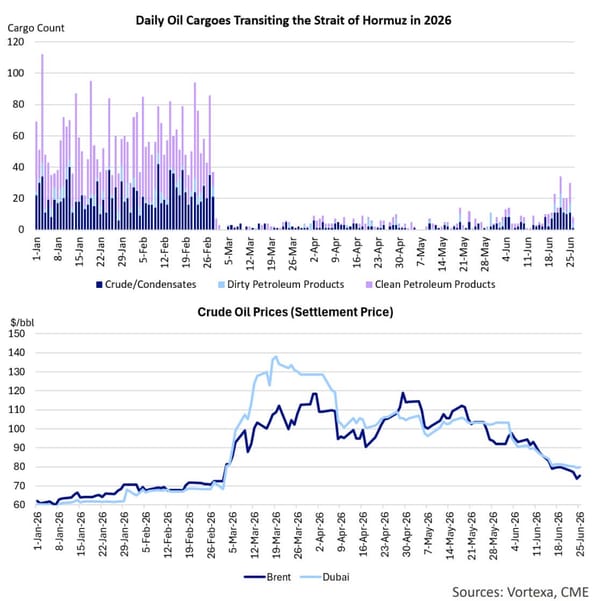

Some of the early changes in the oil and tanker markets were fully expected. First of all, oil prices fell. That was not a surprise. The Memorandum promised a ceasefire and reopening of the Strait of Hormuz, the key chokepoint for Persian Gulf exports. Brent fell below $79 on June 18 after the interim deal was signed, and today it is trading around $72 per barrel, approximately the same price as on February 27, the day before the Iran war started. While nobody was shocked that oil prices came down, the speed with which crude gave up the war premium did surprise the market. The expectation had been that recovery would take weeks or months. Instead, oil prices are back at prewar levels just nine days after the 60-day Hormuz deal was signed, disrupting expectations of a much slower market recovery.

The reason for the rapid oil price retreat is that oil traders look towards the future. Once traders saw actual tanker movements, an OFAC license lifting sanctions on Iranian oil sales, and Gulf producers preparing July loadings, the market looked through the remaining uncertainty and started discounting future supply. As expected, Iranian oil sales quickly picked up after the US lifted its blockade. On June 22, the US Treasury Department issued Iran General License X, authorizing the production, sale, delivery, and offloading of Iranian-origin crude, petrochemicals, and petroleum products through August 21, 2026. The license also covered practical shipping services such as vessel management, crewing, bunkering, piloting, insurance, classification, salvage, and even U.S.-dollar payments. That mattered because the MoU created a temporary legal corridor for trade.

In addition to Iran, other Persian Gulf producers also started to resume loadings. For example, Saudi Arabia resumed crude loadings at Ras Tanura’s Ju’aymah offshore terminal after nearly four months. The UAE, Qatar and Kuwait are also ramping up exports. Iraq, which was badly impacted by the closure of the Strait of Hormuz (its production plummeted from 3.3 Mb/d to 1.3 Mb/d), is boosting production from the Basra fields in the South of the country to maximum capacity. However, while the fields are coming back, actual export volumes from Iraq's southern Gulf terminals are lagging slightly behind those of Saudi Arabia and the UAE.

How did the tanker market respond to the “reopening” of the Strait of Hormuz? Initially, tanker rates jumped. Everybody suddenly needed ships, but many owners were still holding back, ships were out of position, vessels were queued or trapped, and every voyage carried legal, security, insurance, and route uncertainty. At the same time, even with a deal, hundreds of vessels trapped inside the Gulf could not all leave at once, companies and insurers would wait for safety clarity, mine clearance and navigation-lane issues to be resolved. According to the IMO, an estimated 80 sea mines need to be recovered before the traffic separation scheme in the center of the Strait of Hormuz can be reopened.

that matters most

Get the latest maritime news delivered to your inbox daily.

Despite these uncertainties, traffic through the Strait of Hormuz initially jumped significantly after MoU was signed. However, the IRGC attack on a container ship on Thursday increased doubts again about the safety and security of vessels and crew. Following the attack, the IMO suspended its evacuation plan, intended to help free the vessels and seafarers still stuck in the Persian Gulf. The ongoing uncertainly has kept tanker rates particularly volatile. After an initial spike, rates dropped as owners realized there was a abundance of tonnage and that the Iranians were still trying to control traffic through the Strait of Hormuz. This begs the question: Will the situation ever get back to "normal"?

This market update appears courtesy of Poten & Partners.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.