Automation and Offshoring are Changing the Logistics Industry

The impact of Covid-19 has hastened the pace of technological adoption across industries, leading to widespread job losses and a re-designing of job roles and scopes to accommodate the ‘new normal’ of how business is conducted. The biggest shift this crisis will see is that of jobs being automated and offshored from higher-income countries to lower-income ones, accelerating a transition that has been gradually rising over the last decade.

Such rapid changes have left many workers circumspect about the future of their jobs, and there is a real risk - of which many governments are cognizant of - where the bottom third of wage earners will be left behind after the economic seismic waves generated by this pandemic. That the lower-income is especially vulnerable to forces of automation was noted in a study by the Centre for Business and Economic Research (CBER) and the Rural Policy Institute’s Center for State Policy, Ball State University in Muncie, Indiana. They found that a low risk of automation was associated with much higher wages, averaging about US$80,000 a year whereas occupations with the highest risk of automation have annual incomes of less than $40,000.

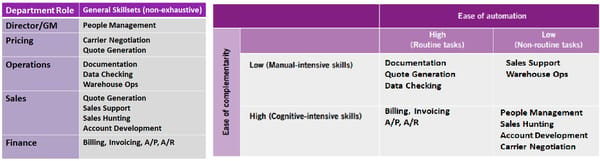

In the shipping industry, the bulk of these jobs most at risk to automation fall mainly into the categories of non-routine tasks and manual-intensive skills as defined by Autor, Levy, Murnane, (2003). They developed a framework which I’ve specifically tailor-fit for job roles within the logistics industry, particularly with third-party logistics companies (3PLs):

Their research findings are further corroborated by Frey and Osborne’s (2013) seminal work, which quantifies the extent to which occupations in the United States can be replaced by modern technology. The main contention is that nearly every occupation can be computerized in the next couple of decades, with the exception of those that involve high amounts of three broadly defined activities – creative intelligence, social intelligence, and perception and manipulation – that currently present automation bottlenecks.

Frey and Osborne concluded, “We find that most workers in transportation and logistics occupations, together with the bulk of office and administrative support workers, and labour in production occupations, are likely to be substituted by computer capital.” They also surmised that occupations requiring knowledge of human heuristics and specialist occupations - skills that the higher income and senior level labor force embody - were the least susceptible to automation

Four Observable Industry Trends

In light of this, we see four discernible trends already taking place. Firstly, 3PLs will continue to consolidate and centralize higher-paying upper management roles through regional geographic clustering. To be more precise, general management, director level and above may - and in some companies are already - taking on P&L responsibilities for more than a single country and stretching their management bandwidth horizontally across geographies of two or three countries.

Secondly, the bulk of upper middle to senior management PMET roles will continue to remain in countries with higher wage structures. However, the roles for this will be few and far between and limited to department manager heads but the scope of responsibility will be increased laterally to take on portions of those previously occupied by Director-level staff.

Thirdly, the majority of operations-related jobs will be offshored to countries with lower labor costs but with a highly educated English-speaking workforce seen in countries like the Philippines and Malaysia. We’ve seen a mix of both customer-facing and non-customer facing roles that move depending on the company’s threshold for cost-cutting and reputation versus maintaining service excellence standards and proximity with their clients. This also encompasses the establishment of Shared Service Centers in low-labor cost countries which specialize in the lower value job tasks on the spectrum, like billing.

Lastly, sales activities continue to be front and center for top line growth. However, to make them less reliant on the fluctuations of existing business being lost due to salespeople leaving and taking accounts with them, 3PL’s will push towards on-boarding clients on their own booking platforms with the objective of increasing direct retention with the SME client segments, which are defined by tight relationships at the ground level and bespoke service expectations.

that matters most

Get the latest maritime news delivered to your inbox daily.

Ultimately, employees who know how to lead the client on the customer excellence journey from booking to final delivery will always be in demand.

Luke Robert consults for SME and MNC clients in navigating trade tariff agreements and advising on industry-wide regulation and the impact of political and economic trends on their supply chains. He is currently with one of the largest logistics MNC’s in the world. The views expressed here are entirely his own.

The opinions expressed herein are the author's and not necessarily those of The Maritime Executive.