U.S. Needs 100 LNG Ships, 30 Years

The U.S. is expected to change from a net importer of natural gas to a net exporter, with those exports destined for different regions of the world, especially Asia. It’s a development that could see the nation building 100 new ships, a prospect that the Government Accountability Office says could take 30 years.

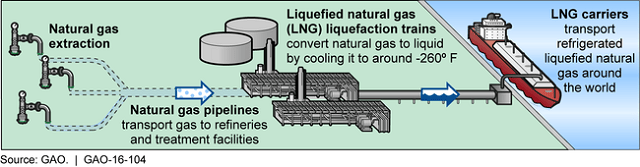

Five large-scale U.S. liquefaction facilities, necessary for conversion of natural gas to LNG, are under construction with a projected capacity to export more than 12 percent of U.S. natural gas production in 2020. According to representatives from these five facilities, their liquefaction capacity has already been sold mainly through 20-year contracts and their customers are responsible for transporting the LNG to export markets.

Based on estimates from these liquefaction facilities, transport of the full capacity of these liquefaction facilities will require about 100 or more LNG carriers.

Currently operating LNG carriers are nearly all foreign built and operated. LNG carriers have not been built in the United States since before 1980, and no LNG carriers are currently registered under the U.S. flag.

The proposed requirement to transport exports of LNG via U.S.-built-and-flagged carriers currently under consideration by Congress could expand employment for U.S. mariners and shipbuilders if it does not reduce the expected demand for U.S. LNG. According to representatives of U.S. mariner groups, between 4,000 and 5,200 mariners would be needed to operate the estimated 100 LNG carriers needed to transport the five U.S. facilities' full capacity of LNG once the five are fully operational.

Based on the current capacity of U.S. shipyards, building 100 carriers would likely take over 30 years, with employment in U.S. shipyards increasing somewhat or becoming more stable, according to shipyard representatives.

Department of Defense officials have indicated that any policy or requirement that increases and stabilizes jobs in the U.S. maritime industry could support military readiness. However, according to industry representatives, U.S. carriers would cost about two to three times as much as similar carriers built in Korean shipyards and would be more expensive to operate.

The U.S. Government Accountability Office (GAO) has released an analysis indicating that these costs would increase the cost of transporting LNG from the United States, decrease the competitiveness of U.S. LNG in the world market, and may, in turn, reduce demand for U.S. LNG.

Additionally, limited availability of U.S. carriers in the early years of construction may decrease the amount of LNG that could be exported from the United States for a period of time, leading customers to seek alternate sources. Further, a reduction in the level of expected U.S. LNG exports could impact the broader U.S. economy, including potential job and profit losses in the oil and gas sector.

More than 30 companies have received approval for large-scale exports of U.S. LNG beginning in 2015 or 2016 via LNG carriers.

that matters most

Get the latest maritime news delivered to your inbox daily.

Congress is considering whether to propose legislative language that would require U.S. LNG be exported via U.S.-built-and-flagged carriers with the goal of supporting U.S. shipbuilders and mariners.

The GAO report is available here.